Feb 27, 2026

How Much Will My Insurance Increase After a Car Accident?

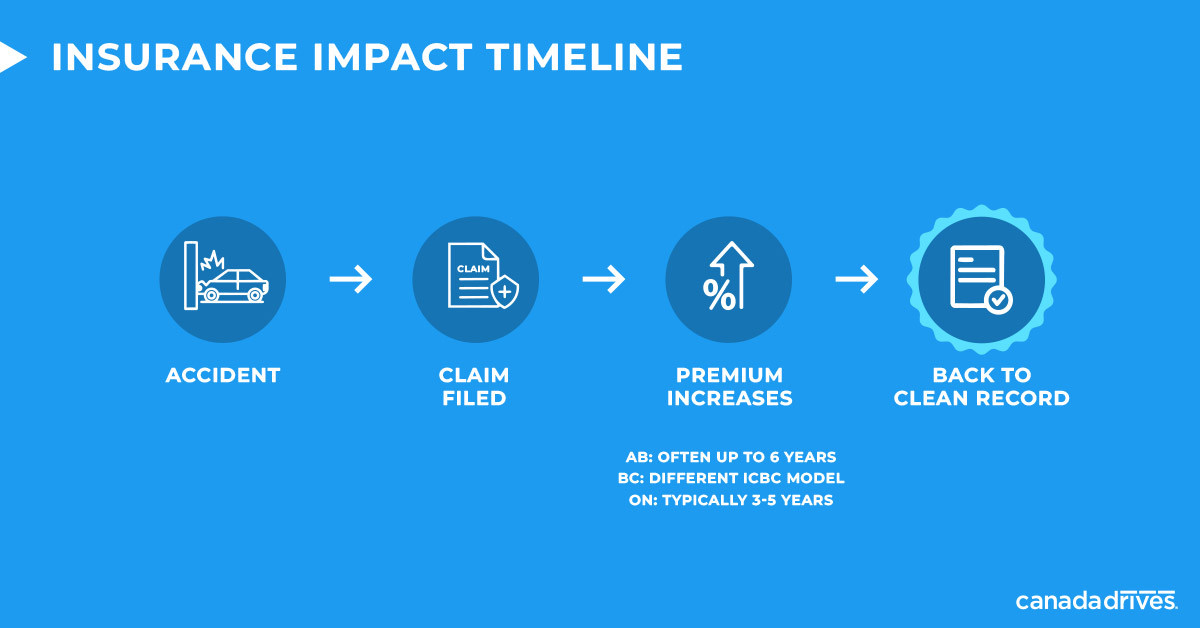

After a car accident, your car insurance premiums can rise—but the size and length of the increase depend on fault, your coverage, and your province.

TL;DR

Car insurance rates aren’t raised by a single universal formula. Insurers price risk using many factors (including your driving record, claim history, where you live, what you drive, your coverage choices, and your deductible).

If you’re at fault, expect higher insurance premiums at renewal—often in the range of 20% to 50% or more, depending on your insurer and your record.

In Ontario, a “minor at-fault accident” that meets very specific criteria (including damages under $2,000 per vehicle and paid by the at-fault driver) generally can’t be used to increase your premiums, with limits on how often that protection applies.

How long the accident’s effects can last varies by province and insurer—commonly three to five years in many situations, but up to six years in many provinces for at-fault accidents, and up to a 10-year scan period for at-fault crashes in B.C.'s ICBC pricing model.

Key Takeaways

- A car accident’s potential impact on your insurance premium hinges on how much fault is assigned to you (including shared-fault scenarios), your claim history, and policy details like collision coverage and deductible.

- Not-at-fault crashes are less likely to raise your base rate, but a claim can still affect discounts with some insurers, so the financial impact isn’t always “zero.”

- Ontario’s Fault Determination Rules require insurers to assign fault using standardized rules, and the rules explicitly say fault is determined without reference to weather conditions or road conditions (among other factors).

- Insurers offer endorsements (sometimes called riders) that can reduce the accidents impact—such as collision forgiveness / accident forgiveness—if you qualify and have it in place before the accident.

- A clean driving record and time are the biggest “reset buttons”: the longer you keep a clean record after the accident, the more likely your premiums will gradually improve once the accident ages out of the lookback window your insurer uses.

How Much Will My Insurance Increase After a Car Accident?

Insurance companies use specialized formulas to estimate the risk you represent, and that’s what drives your insurance premium. Because every insurer weighs inputs differently—and provinces have different rules—there’s no single, solid answer to “how much will my insurance go up after an accident?”

A helpful way to think about this is to separate the immediate costs from the longer-term costs:

Immediate out-of-pocket: things like your deductible (what you pay before insurance pays the rest) and any amounts not covered by your chosen coverage.

Longer-term: changes to car insurance premiums (and sometimes eligibility for certain discounts or endorsements).

Understanding the accident types that impact insurance

A practical starting point is the same one in the original post: at-fault vs. not-at-fault accidents.

At-fault accidents are crashes where your actions are deemed partially or fully responsible. Not-at-fault accidents are those where you’re found 0% responsible. Real-world examples can include getting rear-ended while stopped (often not at fault) versus sliding off the road in winter conditions (often treated as at fault, depending on the facts and province).

What is an at-fault accident?

An at-fault accident is a crash where you’re assigned some level of responsibility—sometimes all of it, sometimes shared with the other driver (or multiple parties).

This “shared responsibility” point matters for premiums because it’s not always a simple yes/no:

In B.C., responsibility can be split (for example 25%, 50%, or 75% responsible), and even partial responsibility can still affect what you pay.

In Ontario, insurers determine the degree of fault according to standardized Fault Determination Rules (and those rules address everything from rear-end collisions to chain reactions involving multiple vehicles).

Who decides fault, and how much fault can you be assigned?

In Ontario, insurers must determine fault “in accordance with these rules” under the Fault Determination Rules.

One detail many drivers miss: Ontario’s rules state that fault is determined without reference to “weather conditions” and “road conditions” (among other factors like visibility and pedestrians’ actions). That means the rules focus on the defined scenarios rather than debating whether ice, rain, or poor visibility “made it happen.”

In B.C., ICBC describes responsibility assessment as a process that can involve statements, witnesses, police reports, and the rules of the road. It also explicitly recognizes partial responsibility and explains that responsibility can be shared when evidence is conflicting or insufficient.

So am I off the hook for not-at-fault accidents?

Often, yes—but not always in the way people expect.

In B.C., ICBC states that if you’re not responsible for a crash in B.C., your claim will not impact your insurance premiums because you weren’t responsible.

However, even when you’re not at fault, the original article noted a common “gotcha”: some insurers apply a claims-free discount, and if an accident results in a claim (at fault or not), that discount can be removed—potentially increasing your premium even when you did nothing wrong.

That distinction is crucial for understanding real-world outcomes:

Not-at-fault does not necessarily mean “no claim was made.”

A claim can still change how discounts apply, which can change what you pay.

At-fault claims free meaning

Drivers often see the phrase “at-fault claims-free” (or similar wording) in quotes, broker conversations, or discount descriptions. In plain English, it usually means you haven’t had any claims where you were found responsible—often within whatever lookback window your insurer uses to price risk.

Why it matters:

Some pricing models and discounts explicitly improve with each year you remain crash-free. For example, ICBC says each year you remain crash-free, your driver factor improves.

Separate from “at-fault claims-free,” some insurers also market claims-free rewards based on claims-free years more generally.

The practical takeaway: if your goal is a clean record (and not just avoiding tickets), minimizing at-fault incidents—and being thoughtful about when to submit claims—can reduce the longer-term financial impact.

No-fault insurance: what it is (and why fault still matters)

“No-fault” can be confusing because it sounds like “no one is at fault.”

In Ontario, no-fault insurance is commonly explained as each driver dealing with their own insurer for benefits and vehicle damage claims, regardless of who caused the collision, while insurers still investigate fault using the Fault Determination Rules.

In other words:

No-fault changes who you claim with (often your own insurer).

It does not eliminate fault as a concept—fault can still affect what coverage applies and what happens to your future premiums.

The coverage pieces that usually drive costs after a crash

If your goal is to predict how your car insurance premiums might change, the coverage you carry matters almost as much as the accident itself.

Collision insurance / collision coverage: generally covers repairing or replacing your car if you hit another car or object, and may be mandatory in some contexts; it’s also commonly referenced as coverage you might drop when a vehicle’s resale value is low.

Deductible: the portion of the claim you agree to pay before the insurer pays the rest. A higher deductible often lowers premiums, but increases out-of-pocket costs after an accident.

What this means after an at-fault accident:

You may pay your deductible to repair your own vehicle under collision coverage (or the equivalent structure in your province).

You may also face higher insurance premiums at renewal because the accident changes your risk profile.

So, how much will my rates go up after an accident?

There’s still no one-size-fits-all number, because many factors affect the result—your province, how much fault you were assigned, your clean driving record (or lack of one), your claim history, the vehicle you insure, your coverage, and the deductible you chose.

That said, multiple insurance-industry sources commonly describe at-fault premium increases in the neighborhood of 20% to 50% (or more), depending on your prior record and the insurer’s rules.

If you’re in B.C., ICBC’s guidance is especially direct: if you’re more than 25% responsible, your Basic insurance premiums will likely go up at renewal (unless you have a long, claim-free record), and optional coverages like collision can go up too.

Ontario’s minor at-fault rule and the “$2,000” threshold

Ontario has a consumer protection that can be easy to misunderstand.

Ontario’s consumer guidance from the Financial Services Regulatory Authority of Ontario explains that insurers can’t use a qualifying “minor at-fault accident” (occurring on or after June 1, 2016) to increase your premiums. The criteria include: no injuries, no insurer payment made, and damages under $2,000 per vehicle that were paid by the at-fault driver, with limits on how often this can apply.

This is why two drivers with the “same accident” can see totally different outcomes:

If the accident does not meet those criteria, insurers may apply a surcharge, and your premiums can remain higher for multiple years.

If it does meet the criteria, you may be able to avoid a premium increase from that incident (even though it happened).

How long does an accident stay on your insurance in Ontario?

Two timelines matter: how long your premiums are affected, and how long the incident remains visible in underwriting/rating lookbacks.

For many Ontario drivers, filing a claim for a car accident will most likely increase premiums for three to five years, according to CAA’s Ontario auto insurance FAQ guidance.

But insurers can use at-fault accidents as a rating factor for longer than that in many provinces. For example, Intact notes that in most provinces, at-fault accidents can stay on your record for up to six years.

A practical way to interpret this:

In Ontario, you might feel the biggest premium change over three to five years in many common situations.

But the accident can still be relevant for pricing and underwriting decisions up to six years in many cases, depending on the insurer.

How long does an accident stay on your insurance in Alberta?

Alberta is a private insurance market, but the provincial government’s consumer guidance on rate caps gives a clear clue about the lookback that matters for pricing.

For Alberta’s “good driver” rate cap in 2025 and 2026, a driver is not considered a “good driver” if they have an at-fault accident in the last 6 years (among other criteria).

So, while each insurer’s exact rating can vary, an at-fault accident in Alberta can have a potential impact for up to six years in at least one important pricing/eligibility context tied to renewals.

How long does an accident stay on your insurance in B.C.?

In B.C., ICBC publishes unusually specific details about how crash history is used.

ICBC describes a “crash history scan period” and explains that it has introduced a ten-year scan period for at-fault crashes. It currently looks back to at-fault crashes from March 1, 2017, and will keep scanning back to that date until 2027; after that, it becomes a rolling 10-year lookback at each renewal.

Practically, that means an at-fault crash can influence your pricing for a long time—up to a decade—depending on where it falls relative to the scan period rules in effect at your renewal.

Can you prevent the increase (or reduce it)?

Sometimes—if you plan ahead, and if your policy and province allow it.

Collision forgiveness / accident forgiveness: The Government of Canada’s consumer guidance describes collision forgiveness as an optional feature (an endorsement/rider) that keeps your premium from increasing after your first at-fault accident.

But you typically need to have it before the accident. Insurers commonly treat accident forgiveness as something you add in advance; it’s not something most people can buy after the crash to erase the premium impact retroactively.

In B.C., ICBC also notes that repaying a claim can sometimes make financial sense so it won’t affect your future premium (typically in less serious crashes where the math works out).

Final thoughts

If you’re trying to estimate the accidents impact on car insurance premiums, focus on three things:

Fault and how much fault you were assigned (especially if there are multiple parties).

Coverage structure (especially collision coverage and your deductible) and whether your policy includes an endorsement like accident forgiveness.

Time and your record: keeping a clean driving record after the accident can help your premiums recover as the accident ages out of rating windows (three to five years in many common cases, up to six years in many provinces, and up to a 10-year scan period in B.C.).

FAQ

Will my insurance premiums go up if I’m not at fault?

It depends on your province and insurer. In B.C., ICBC states that a not-at-fault claim won’t raise your premiums, but in other provinces a claim may still affect discounts like a claims-free discount.

How much can an at-fault accident raise my insurance premium?

There’s no fixed amount, but increases of 20% to 50% or more are common. The exact impact depends on your driving record, your insurer’s policies, and how much fault you were assigned.

What does “deductible” mean, and will I have to pay it?

A deductible is the amount you pay before your insurer covers the rest of a claim. Whether you pay it depends on your coverage and fault, and it commonly applies under collision coverage.

Does collision coverage matter if I’m at fault?

Yes. Collision coverage helps pay for repairs to your vehicle if you hit another car or object. If fault is shared, it may cover the percentage you’re responsible for, depending on your policy.

Can I buy accident forgiveness after an accident?

Usually not. Accident forgiveness must typically be added to your policy before an at-fault accident occurs, and eligibility varies by insurer and province.

Is paying out of pocket ever better than filing a claim?

Sometimes. For small claims, it may make sense to compare the deductible and potential premium increases before filing. Ontario also has protections for certain minor at-fault accidents under $2,000 per vehicle.

How long will my car insurance rates stay higher after an accident?

In Ontario, premiums often increase for three to five years after a claim. In many provinces, insurers may look back up to six years for at-fault accidents, while B.C. uses a longer crash history model.

Do bad road conditions automatically reduce fault?

Not necessarily. In Ontario, fault is determined under specific rules and does not consider weather or road conditions.

People Also Ask

Do all accidents increase car insurance rates?

Not always. At-fault accidents are more likely to raise car insurance rates, while not-at-fault claims may not increase your insurance premium, depending on your province and insurer.

How do insurers decide how much fault I have?

Fault is determined using provincial rules and the details of the collision. In cases with multiple parties, insurers assess how much fault each driver shares based on set guidelines.

Will my car insurance premiums ever go back down?

Yes. If you maintain a clean driving record and avoid further claims, your car insurance premiums typically decrease over time once the accident ages off your record.

Can one accident affect my clean driving record?

Yes. An at-fault accident can remove a clean record status and may lead to higher insurance premiums for several years.

Does a small claim still impact my insurance?

It can. Even minor claims may have a financial impact, especially if they affect discounts or claims-free status, which can influence future car insurance rates.

Related Prompts

How do I decide whether to file a claim or pay out of pocket after a minor collision?

What questions should I ask my insurer about accident forgiveness and claims-free discounts before renewal?

How does collision coverage differ from comprehensive coverage in Canada?

What’s the difference between a not-at-fault crash and a no-fault insurance system?

How do fault determination rules work in Ontario for common scenarios like rear-end collisions and parking lot crashes?

How does ICBC’s driver factor work, and how does it change after a crash-free year?

What are the best ways to lower my insurance premium without sacrificing critical coverage?

How do car insurance rates change when I switch vehicles after a write-off?

About Canada Drives

Canada Drives helps Canadians get pre-approved for vehicle financing before they start shopping. Our online application matches drivers with local dealerships that have vehicle options for all credit situations, including bad credit or limited credit.

With one simple pre-approval, you can avoid wasted time at the dealership and shop with confidence knowing exactly what you're approved for.